Oil Pipelines, Cell Towers, and Bottling Lines: What Healthcare Can Learn from Africa’s Capital Giants

What makes an industry capital intensive? According to Investopedia, a capital intensive industry is a sector that requires significant investment to produce goods and services. Typical sectors associated with the “capital intensive” label are oil production, telecommunications and automobile manufacturing. Healthcare, however, rarely appears in the same sentence as ‘capital intensive’, and healthtech almost never does. This article aims to make a case for why the healthcare industry in Africa, particularly in Nigeria, can and should be considered capital intensive, at least in the short- to medium-term, and the treasure trove of lessons the healthcare industry could learn from key African capital giants: oil, telecoms, and food and beverage.

But first, let’s properly define what a capital intensive industry is. There are three main factors or criteria that make an industry capital intensive. First, it requires large investments in physical assets (e.g., plants, machinery, infrastructure) relative to labour. Second, it has high fixed costs and long payback periods, meaning it needs consistent demand to cover depreciation and operating costs. Lastly, it typically has higher barriers to entry, because new players must raise significant capital before they can compete.

African healthcare meets all three criteria.

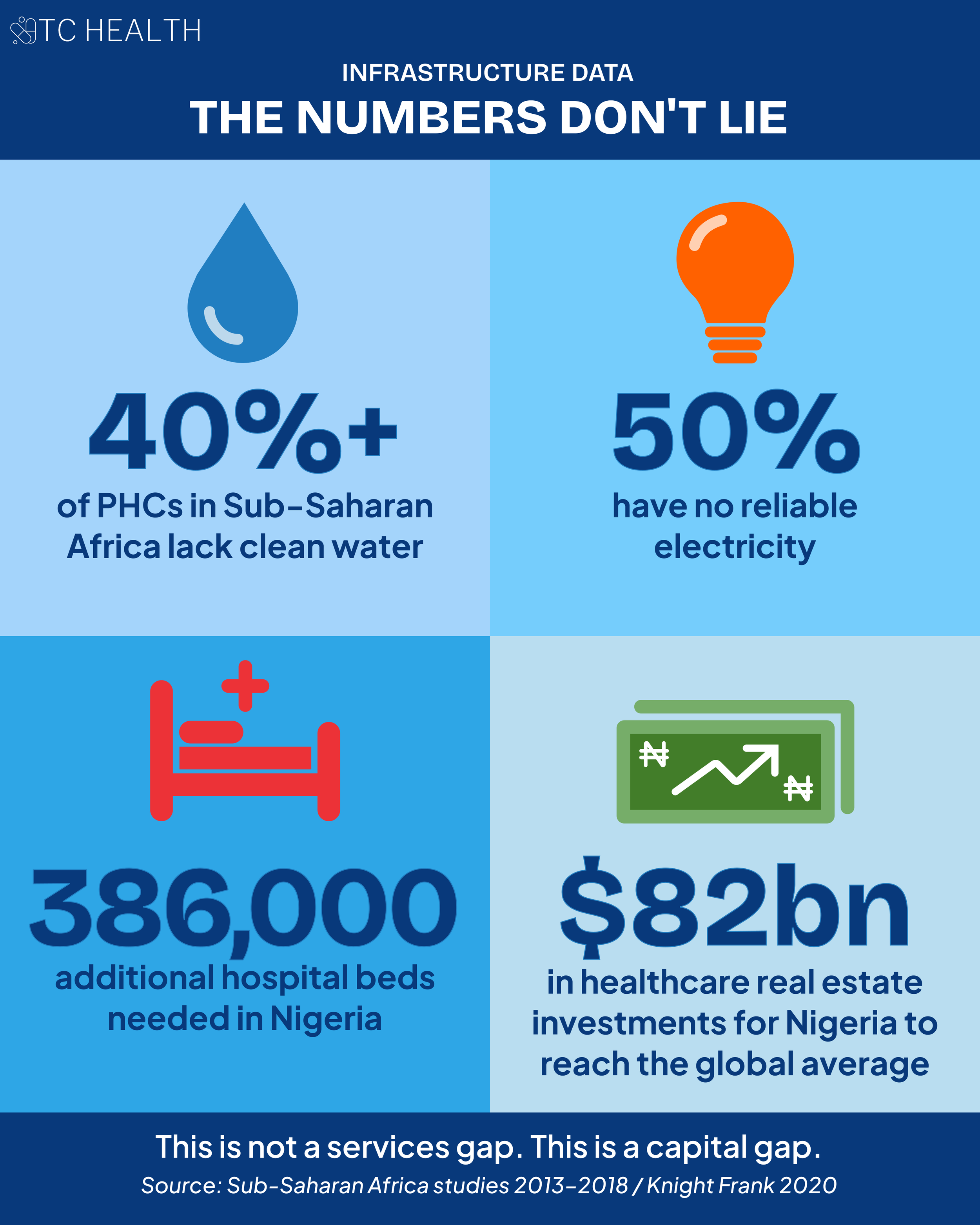

Studies in Sub-Saharan Africa found that over 40% of primary healthcare facilities lack clean water, 15% have no electricity at all, and 50% lack reliable electricity services. Africa faces significant deficits in financing for healthcare infrastructure. Currently, African governments spend roughly $4.5 billion in capital each year–far below the estimated $26 billion in annual investments needed to meet evolving health needs over the next decade. A 2020 Knight Frank report indicated that, except for South Africa, all African countries fall short of the global average ratio of 2.7 hospital beds per 1,000 people and require significant investments in healthcare infrastructure to catch up with the rest of the world. Nigeria, for instance, would need 386,000 additional beds and $82 billion of healthcare real estate investments to reach the global average. Despite this significant infrastructure gap, the Nigerian government released only 0.016% (or ₦36 million) of the ₦218 billion appropriated for health capital projects in 2025 – a figure that has dropped from 70% in the past 5 years, according to this report.

RELATED: Bridging the Funding Gap in Healthcare Infrastructure

Another significant challenge in African healthcare is the human resource crisis. Africa is home to just 3% of the world’s healthcare workers, despite bearing a quarter of the global disease burden. This gap is caused and exacerbated by the medical brain drain plaguing several African countries. According to the Nigerian Federal Ministry of Health’s statistics report, over 43,000 health workers migrated abroad between 2023 and 2024, representing a 200% surge across all cadres. To combat this shortage of healthcare workers, significant investments are required in healthcare infrastructure to improve working conditions, and in medical training institutions to replenish the number of doctors and nurses emigrating to other countries.

RELATED: The Signs & Symptoms of Nigeria's Medical Brain Drain

So far, we’ve shown that African healthcare meets the first criterion of a capital-intensive industry. But when we look closer into the nature of the investments that are needed—refurbishing existing hospitals and clinics, building new centers, acquiring multi million-dollar equipment, and making multi million-dollar endowments in universities, among others—we see that these all require high fixed costs and long payback periods. Current demand and willingness to pay remain relatively low across the healthcare sector due to economic challenges and high informal sector participation (>70%). As a result, the repayment horizon for these investments will almost definitely be long term.

To address the final criterion of high barriers to entry, we will use a real-world example. mDaaS, a healthtech company, was originally founded in 2016 as an importer of refurbished medical diagnostic equipment in Nigeria. The company had a relatively simple business model at launch: bring in equipment from the US and provide technical support on the ground in Nigeria. However, the founders soon realised the economics of the business model were not scalable because a large proportion of the market could not afford nor justify the upfront investment for diagnostic equipment even though the unmet need was there. As a result, in 2017 the company pivoted to providing diagnostic services to hospitals and clinics, and opened its first medical centre. Today, it has expanded to 26 centers all across Nigeria, operating these centers under the company’s patient-facing brand, BeaconHealth Diagnostics.

This should be treated as a significant barrier to entry. Building brick-and-mortar infrastructure at scale is out of reach for many firms, particularly technology companies whose value propositions depend on asset-light models. The structural conditions make this unavoidable: with over 70% of Nigeria’s total health expenditure paid out-of-pocket, there is no reliable payer infrastructure for operators to underwrite capital costs against. The market simply does not have the financial architecture that allows asset-light models to sustain themselves.

In Sub-Saharan Africa, healthcare and healthtech companies are often forced into this exact reality, as infrastructure gaps limit both growth and competition. The consequences are visible at both ends of the market. Among established providers, ~20% of Nigeria’s small and medium-sized private hospitals shut down in 2024, overwhelmed by the capital demands of operating in an environment without reliable power, stable FX, or functioning supply chains. Among newer entrants, the attrition is equally stark: only 24 Nigerian healthtech funding rounds were disclosed in 2023 and 2024 combined, the same number recorded in 2021 alone. And in 2024, not a single growth-stage round was announced. To tie it all together, this analysis argues that due to infrastructure deficits, healthtech companies in markets like Nigeria and Ghana are forced into “infrastructure substitution” and “capital trap” models where founders must build nearly all the infrastructure they must operate their businesses in, significantly limiting scalability.

So far, we have made the case that African healthcare can and should be classified as a capital-intensive industry. Deep infrastructure gaps create a substantial barrier to scale for any healthcare business. Yet this is not all doom and gloom. Nigeria and several other African countries have successfully scaled capital-intensive industries that now anchor their economies. We’ve scaled oil. We’ve scaled telecoms. We’ve scaled food and beverage (F&B). The result is a rich set of transferable lessons that could open new pathways for growth in African healthcare. So, it’s time to scale healthcare.

In this article, we use Nigeria as a case study—one of Africa’s largest and most complex healthcare markets—to explore these 3 capital giants and answer a few key questions:

What funding models enabled scale?

What policies enabled scale?

What partnership models enabled scale?

What funding models enabled scale? (4-min read)

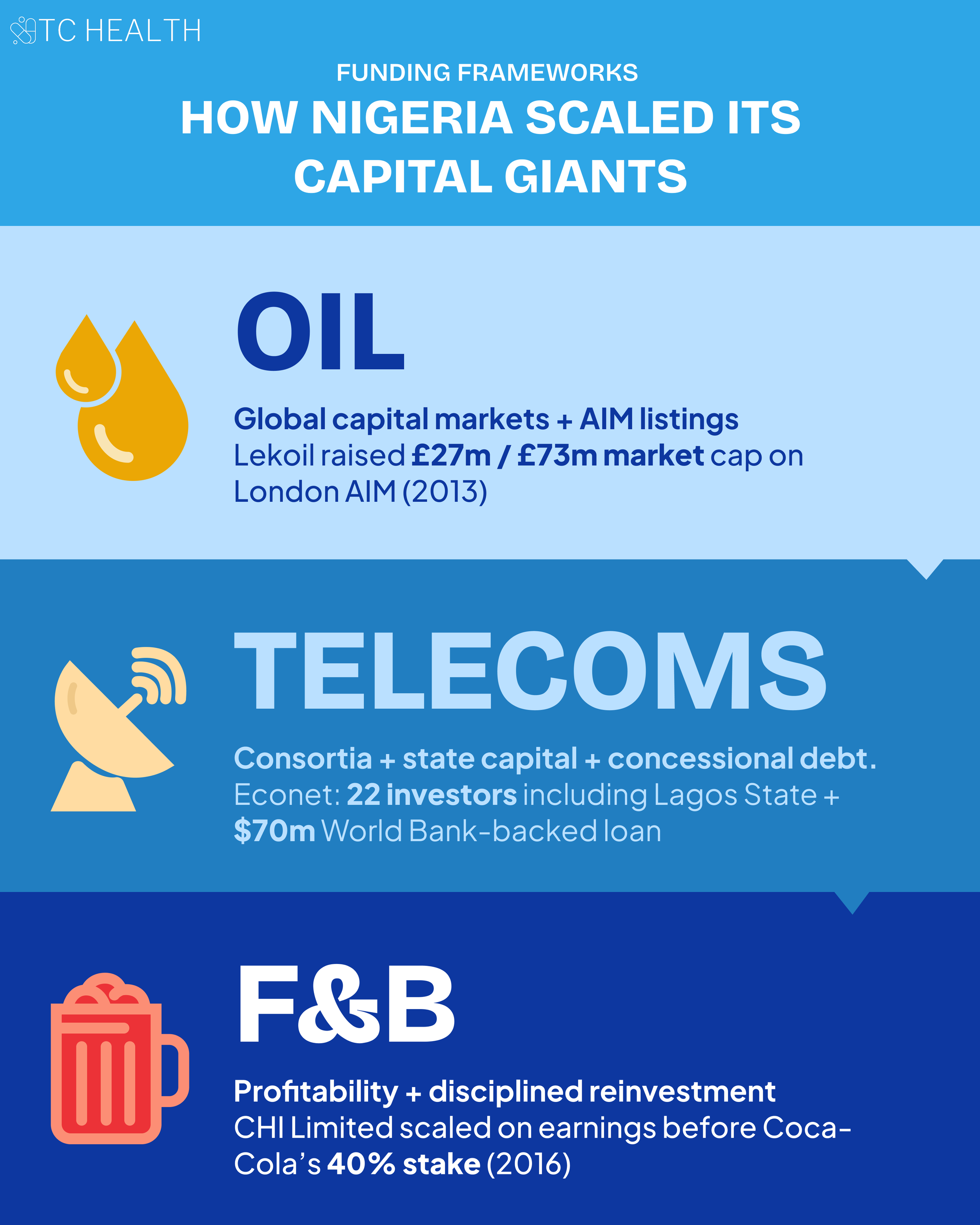

Let’s start with Nigeria’s powerhouse industry: oil. The oil industry has colonial era roots. In the early 1900s, smaller British-registered companies like the Nigerian Bitumen Corporation were unable to scale due to their small size and the pressures of World War 1. Larger international companies like the Shell-BP consortium came in the 1930s, and drilling and exporting began in the 1950s and 1960s, with other large international firms like Mobil and Chevron entering the market. By the early 1970s, in the post independence era, the Nigerian government nationalised the oil industry by forming the Nigerian National Oil Corporation (NNOC), which later merged with the Ministry of Petroleum to become what we know as the Nigerian National Petroleum Corporation (NNPC) today.

As time went on, indigenous companies began to enter into the oil industry. But how did they scale? Let’s deep dive into one specific company, Lekoil, to extract some key learnings about early stage funding. Lekoil was founded in December 2010 and struggled initially to raise capital and scale. However, in May 2013, three years after it was founded, Lekoil successfully listed on the Alternative Investment Market (AIM) in the United Kingdom, raising net proceeds of ~£27m with a market cap of £73m, a record amount for a new entrant Exploration and Production (E&P) company on AIM. Launched in 1995, the AIM is a sub-market of the London Stock Exchange that allows companies that are smaller, less-developed, or want / need a more flexible approach to governance to float shares with a more flexible regulatory system than is applicable on the main market.

This represents an alternative pathway for raising capital for a smaller company. Dr. Ikpeme Neto, expanded on this point further in his article arguing for African startups to explore global IPOs by looking to European public markets. He cites an example of a Kenya-based startup, Mdundo, that underwent a global IPO in a European market, Nasdaq First North Denmark, in 2020, raising $6.4 million on a valuation of $9 million despite annual revenues of only ~$54k. The oil sector’s experience makes one thing clear: scaling a capital-intensive industry in Africa requires pathways beyond patient capital. Creative financing structures and access to global capital markets could present a uniquely attractive pathway.

Telecoms presents a contrasting but equally instructive case, where funding scale was unlocked through domestic and state investors and concessional capital via development finance institutions.

When the telecoms industry was opened up to private sector players via GSM bids in the 1990s and early 2000s (we will explore this further in the policy section), Econet (now Airtel Nigeria) capitalised on this opportunity by developing a consortium of Nigerian institutional and high net worth investors, including Lagos and Delta State. A little backstory: To qualify for the original GSM bid, a member of the bidding consortium had to be an experienced GSM operator. Econet Wireless, the leading telecoms provider in Zimbabwe today, met the requirements because of its experience in Zimbabwe and Botswana. So the original consortium included 22 investors, including state governments, local banks, and high net worth individuals, bidding for a licence cost of $285m—the most expensive issued in Africa at the time.

Econet’s network rollout was further supported through a combination of insured equity and external debt, including a $70 million loan from Ericsson Credit AB backed by the Multilateral Investment Guarantee Agency (MIGA), a member of the World Bank Group. MIGA was established to encourage foreign investment in emerging markets by providing political risk guarantees that protect investors and lenders against risks such as expropriation, conflict, or breach of contract. In 2002, MIGA provided a $10 million guarantee to support Econet’s equity investment in its Nigerian subsidiary. In practical terms, this meant that part of the capital Econet committed to building its Nigerian operations was protected against certain political and non-commercial risks, making it easier for investors to commit long-term funding to the venture.

For healthcare companies, the lesson is clear. Scale was not achieved on venture capital alone. Scale came from diverse capital sources, strong local investor participation, state involvement, and risk-mitigating instruments from development finance institutions. Healthcare and healthtech companies operating in similarly capital-intensive environments will likely need to pursue a similar mix of equity, debt, public funding, and concessional capital if they are to scale sustainably beyond pilot-stage growth. This is the same conclusion discussed in Season 1, Episode 3 of The Cure, where Dr Neto and Temitope Coker explored why healthtech in Africa will need to look beyond VC toward blended capital structures that include equity, debt, public funding, and concessional finance in order to scale sustainably.

Finally, we can look to the food and beverage industry to explore more fiscally conservative approaches to scale from a key indigenous player—CHI Limited (Chivita|Hollandia). CHI Limited was incorporated in 1980 to plug a key gap in the market for locally made, high-quality food and beverage products tailored to Nigerian tastes after the oil crashes in the 1980s that made FX risks and imports challenging. Funding in the early years was mostly private capital and reinvested earnings / profits. The company used profits to invest in processing plants, automated bottling lines, and extensive distribution infrastructure, enabling it to scale.

The lesson here is straightforward. Scale does not always require aggressive external fundraising. In the case of CHI Limited, growth was driven by profitability and disciplined reinvestment into core infrastructure and distribution. For African healthcare and healthtech companies, this suggests that long-term impact may be built less on large VC rounds and short-term valuations, and more on sustainable, profitable models that can compound and endure over time.

What policies enabled scale? (5-min read)

Government intervention through favourable policy is an almost universal facet of capital giants. In every capital-intensive industry, scale has not emerged from capital alone, but from policies that reduced risk, incentivised private investment, and aligned public and private interests. Without deliberate government intervention, the upfront costs and long payback periods in sectors like oil and telecoms would have made large-scale private investment unviable. Policy, in these cases, did not replace the market; it made the market possible.

Once again, we start with oil. As the Nigerian oil industry is nationalized via the NNPC today, a significant proportion of business operations are controlled by the government. One such mechanism widely used in the industry are production sharing contracts (PSCs). PSCs enable both parties—the government of the oil producing country and the oil company—to share the risks and rewards of oil exploration and exploitation activities. Essentially, within a PSC, the government as the owner of the mineral resources engages an oil company as a contractor to provide technical and financial services for exploration and development operations. This could be seen as a “win-win” setup as the government no longer needs to meet its periodic cash call obligations to joint ventures, while the oil companies as operators embrace the varying degree of fiscal incentives and convenient work programs offered by the PSCs.

One notable, recent PSC was between NNPC, TotalEnergies and Sapetro (an indigenous oil company) for Oil Prospecting Licences (OPL) 2000 and 2001 located in the offshore Niger Delta Basin, two offshore blocks spanning about 2,000 square kilometers. This PSC includes a range of incentives designed to make deepwater exploration and production commercially attractive. First, the signature bonus is set at $10 million, which serves as the initial payment upon contract award, lowering the front-loaded entry costs. Additionally, performance incentives are built into the terms, with production bonuses tied to commercial milestones—specifically 2 million barrels on reaching 35 million barrels of cumulative output and 4 million barrels (or their cash equivalent) on reaching 100 million barrels of production—rewarding delivery on early and scaling phases of development. The contract also establishes clear rules on cost recovery, capped at ~70%, so companies can recoup allowable costs from production before profit sharing. These fiscal terms, combined with a minimum work program and performance guarantees, aim to give investors predictability and reward progress on planned exploration and development activities. Collectively, these provisions help align contractor returns with milestone achievement while also ensuring value flows to the state. NNPC praised this PSC for its potential to bring it closer to achieving its target of three million barrels per day and securing an additional $60 billion in investments by 2030 as part of broader upstream sector growth expectations.

The lesson here for the healthcare sector is not just “more public private partnerships (PPPs)”. Though often an empty buzzword, PPPs can unlock significant growth if more intentional risk-sharing structures that align incentives between government and private operators are applied. In Nigeria’s health sector, elements of this already exist due to low public sector funding and operational capacity: private HMOs manage National Health Insurance Scheme (NHIS) enrollees as contracted partners. Yet the opportunity for structured expansion remains significant. A particularly attractive low hanging fruit is in primary healthcare infrastructure. Only about 20% of Nigeria’s 30,000 primary healthcare facilities are fully functional, meaning 80% can be revitalized via PPPs.

A promising precedent already exists. At the Healthcare Federation of Nigeria 2026 public sector roundtable, a panelist representing the Association of Local Governments of Nigeria (ALGON) described how the organisation partnered with PharmAccess to help private operators reopen long-abandoned, publicly built PHCs in rural and conflict-affected communities. Through a structured model, 15 facilities were operationalised. The initiative reportedly delivered zero maternal deaths over a five-year period in those remote sites and was supported by a Bank of Industry arrangement that enabled providers to be repaid in full. It also revealed the policy constraints on scale. Earlier rules under the Basic Health Care Provision Fund (BHCPF)—Nigeria's premier primary care financing initiative—had explicitly excluded private providers, limiting how far the model could spread. This type of scale would be challenging to sustain in the public sector, where budgets are constrained and incentives are often not aligned with those of private partners. Private operators, by contrast, entered with a commercial lens and applied the efficiency and business discipline needed to turn these facilities around.

There is room to design performance-based contracting models where private operators rehabilitate and manage facilities in exchange for predictable revenue streams such as capitation payments or service-based reimbursements. Just as PSCs in oil rebalanced risk and reward to unlock deepwater investment, healthcare policy can evolve to de-risk infrastructure expansion while safeguarding public interest.

RELATED: Charting a Healthier Course: The State of Nigeria's Primary Care

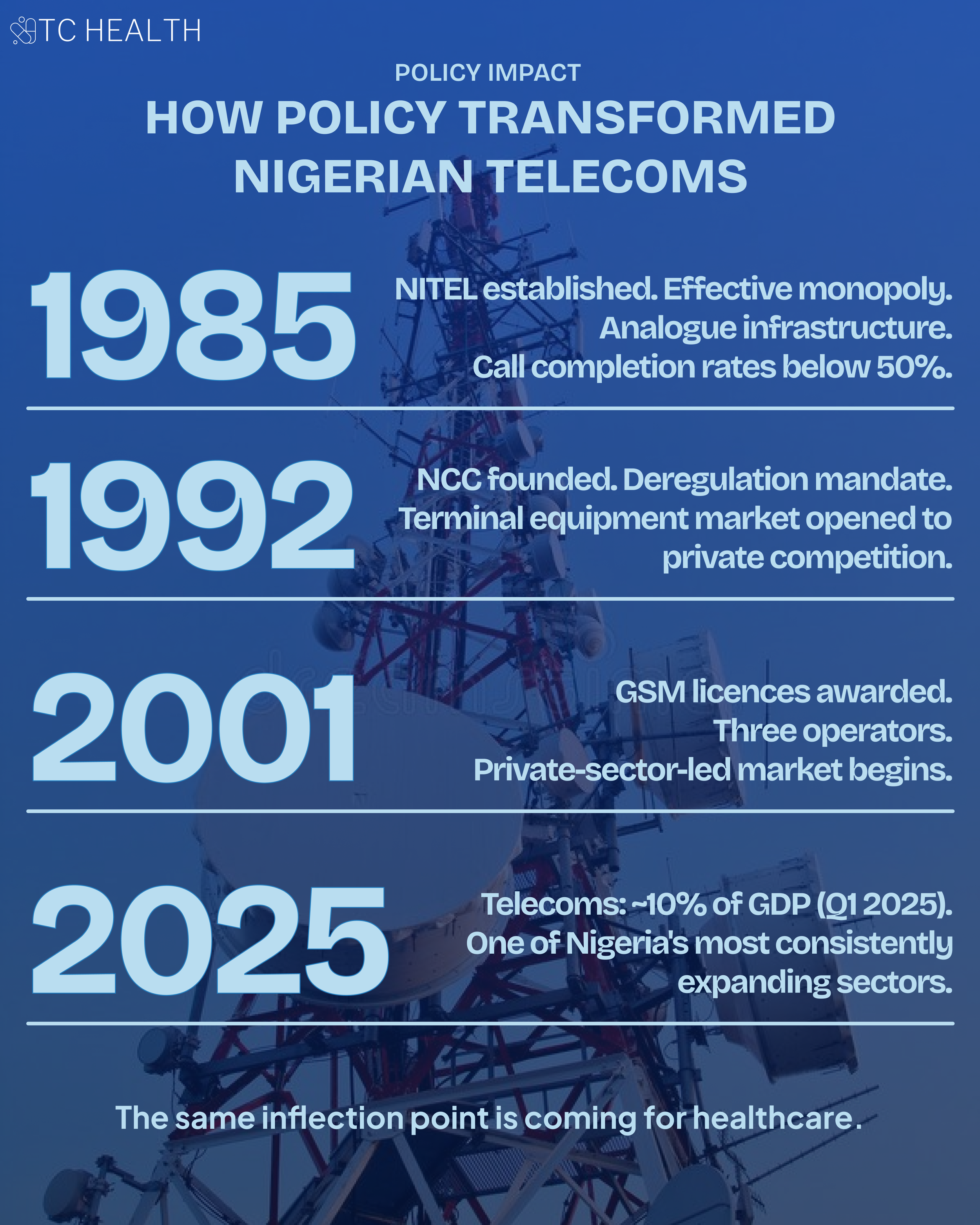

The telecoms industry offers another powerful example of how policy reform can unlock scale. The Nigerian telecoms industry has somewhat of a spotty history. Nigeria Telecommunications Limited (NITEL) was established in 1985 through the welding together of two government entities—the telecoms arm of the Posts and Telecommunications (P&T) department under the Ministry of Communications, and Nigerian External Communications (NET) Limited. NITEL, an effective monopoly at the time, was plagued with poor service delivery—from mostly analogue infrastructure, to inefficient billing systems, and long distance call completion rates below 50%—heralding communication service reforms. As a result, the Nigerian Communications Commission (NCC) was established in 1992 with a mandate for deregulation. The decree establishing the NCC helped to liberalize terminal ends equipment, and gave room for competition and private sector participation. Before liberalization, NITEL often controlled what devices could be connected to the public network, required approvals for specific models, limited imports or sales to approved channels, and occasionally rented equipment to subscribers rather than letting them buy freely. But the NCC’s creation removed these restrictions so private companies and consumers could import, sell, own and connect terminal end equipment (e.g., telephones, fax machines, modems, etc.), and multiple vendors could compete.

The breakthrough came in 2001 with the introduction of the Global System for Mobile Communications (GSM) and the award of renewable GSM licences operating on the 900/1800 MHz spectrum bands. This combination of regulatory clarity, competitive licensing, and technological upgrade transformed Nigeria’s telecoms landscape from a stagnant monopoly into a dynamic, private-sector-led market. Today, telecoms contributes significantly to GDP (almost 10% in Q1 2025) and remains one of Nigeria’s most consistently expanding sectors.

So what’s the lesson for healthcare? In the telecoms industry, technology adoption and innovation was policy-enabled. The GSM revolution did not occur in a vacuum; it was made possible by regulatory frameworks that encouraged competition, clarified licensing, and reduced barriers to entry.

As digital health, telemedicine, and AI gain traction across healthcare systems, scale will depend on whether policy frameworks actively enable innovation while safeguarding patient safety. For example, in 2021 the Pharmacy Council of Nigeria (PCN) introduced Online Pharmacy Regulations that require online sellers to operate under a superintendent pharmacist, register a single licensed internet platform, dispense prescription-only medicines only against a valid physical prescription, maintain delivery audit trails, and meet defined patient-safety standards.

While these measures created a legitimate legal pathway for digital pharmacies where none had formally existed, their design has directly constrained the business models they govern. A legal review of the regulations noted that the physical prescription requirement eliminates the ability to prescribe remotely following an online consultation which is the very value proposition that makes digital pharmacies distinct. It also noted that platforms should "collectively lobby for the review of regulations" to reduce restrictions on their business model and revenue potential. A separate provision, Rule 21(5), appears to restrict operators to a single website, limiting the ability to scale or offer specialised services. More broadly, Nigeria remains one of the few countries on the continent without dedicated telemedicine legislation; as one legal analysis notes, this "disincentivises investment and innovation, ultimately limiting the scalability and sustainability of telemedicine."

However, in recent times, new policies in the digital health space show that the government understands the direction of travel. At the Nigeria Telehealth Conference in November 2025, it was revealed that Nigeria is currently finalising its National Telemedicine Guideline (NTG) to regulate, structure, and scale digital health. The aim of the NTG, which is over 90% complete, is to govern remote consultations, digital record-keeping, and security, creating a standardized framework for practitioners and developers.

Additionally, the Pharmacy Council of Nigeria (PCN) just released new regulations for online pharmacies in March 2026. The new regulations have reversed some of the constraints of the 2021 policy, for example: e-prescriptions from telemedicine are now explicitly valid, and electronic pharmacies may operate without physical premises provided they partner with a licensed physical pharmacy. However, this no-premises partnership model may be less useful than it appears. Roughly 30% of Nigeria’s retail pharmacies are in Lagos and several states have less than 5 community pharmacies each. While this policy provision is designed to enable digital pharmacy reach in underserved communities, requiring a licensed physical pharmacy nearby undermines this goal in some of the most remote communities in the country.

RELATED: From Dispensary to Diagnosis: How Nigerian PBMs & Pharmacies are Bridging the Gap in Primary Care

The constraints most relevant to scalability carried over intact from the 2021 PCN policy. Superintendent pharmacists can still only be registered to a single platform, which limits aggregation. Additionally, aggregator platforms connecting multiple pharmacy providers to consumers must now register as electronic pharmacies themselves, a compliance requirement that did not exist under the 2021 rules.

When Coordinating Minister Prof. Muhammad Ali Pate launched the 2026 PCN regulations, he described them as the end of operating in a grey area. Formalisation and liberalisation are not the same policy instrument. The 2001 telecoms moment worked because it did the latter, clarifying licensing and structuring competition in ways that made investment viable where it had not been before. Nigerian digital health is still waiting for its equivalent.

What partnership models enabled scale? (3-min read)

Partnerships are another consistent thread across capital-intensive industries. In markets where no single player can carry the full burden of capital, expertise, and execution risk, scale is often achieved through structured alliances that combine complementary strengths.

Once again, we start with oil. The Nigerian oil industry is built on layered partnerships between international oil companies, indigenous firms, and the state. A clear example is Sapetro, an indigenous company that was awarded the deepwater frontier acreage OPL 246 during Nigeria’s 1998 bid round. Rather than developing the asset alone, Sapetro partnered with two international oil companies, Total and Petrobras, to execute exploration activities. This collaboration led to the discovery of the Akpo and Egina fields, each with estimated reserves of approximately 500 million barrels. Following discovery, the partnership expanded to include CNOOC, a Chinese-headquartered global energy company, and the consortium jointly undertook field development.

This model illustrates a key principle: indigenous participation does not preclude global partnership. Instead, it is often through these partnerships that local companies gain access to capital, technical expertise, and execution capabilities required to operate at scale. Over time, Sapetro leveraged this model to expand beyond Nigeria into markets such as Benin, Mozambique, and Madagascar, demonstrating how partnerships can serve not just as a mechanism for entry, but as a platform for regional growth.

A similar pattern emerges in telecoms. As discussed earlier, Econet’s entry into Nigeria was built on a consortium model that combined local investors, state participation, and an experienced foreign operator. But beyond capital, Econet itself played a distinct role within the partnership as the technical partner and operator, bringing the expertise required to build and run the network. Econet was responsible for deploying and operating the infrastructure, and in return, received approximately 3% of turnover as management fees, which was standard industry practice at the time.

This structure highlights an important nuance in partnership models: not all partners contribute capital. Some contribute capability. By separating financial ownership from operational expertise, the consortium was able to align incentives across investors, operators, and the state, enabling rapid deployment of capital-intensive telecom infrastructure. The lesson here is that scale was not achieved by any single actor, but through coordinated partnerships that combined capital, technical expertise, and execution capacity.

For healthcare, this model of capability-driven partnerships is already beginning to take shape. A recent example is Sygen Pharma, an indigenous pharmaceutical company, which partnered with Canadian firm ORx Pharmaceuticals in August 2024 to form a joint venture, Sygen-ORx Biosciences. The collaboration brings together ORx’s drug development expertise and technology with Sygen’s local market knowledge to develop improved and locally relevant formulations of generic medicines, including anti-malarials, antibiotics, and anti-diabetes treatments. As discussed in Season 1, Episode 1 of The Cure with Charles Ogunwuyi, CEO of Sygen Pharma, this type of partnership reflects a broader shift: African healthcare companies do not need to build every capability in-house. Instead, like indigenous oil firms partnering with international operators, they can combine local presence with global technical expertise to accelerate product development, improve quality, and scale access to essential medicines.

In the food and beverage industry, partnerships have taken a slightly different form, evolving from collaboration into acquisition. CHI Limited provides a strong example. After building a successful indigenous brand through local manufacturing and distribution, the company attracted strategic investment from The Coca-Cola Company, which acquired a 40% stake in 2016 and completed a full acquisition in 2019. More recently, in 2025, CHI was sold to UAC of Nigeria PLC, a major Nigerian industrial conglomerate. This evolution highlights an important dynamic: partnerships are not always static. They can serve as pathways to acquisition, consolidation, and further scaling within larger ecosystems.

For healthcare, the lesson is not limited to public-private partnerships. While PPPs play an important role, particularly in infrastructure, the experiences of oil, telecoms, and F&B suggest that private-private partnerships and strategic alliances are equally critical.

First, vertical partnerships across the value chain can unlock scale. In the United States—itself a highly fragmented healthcare market—the most instructive recent examples have come not from startups but from incumbents deliberately collapsing the distance between adjacent parts of the system. In 2018, CVS Health, one of the country's largest pharmacy and retail health chains, acquired Aetna, a major health insurer, for approximately $69 billion, combining insurance, pharmacy benefits management, and retail care delivery under one roof. The same year, Cigna acquired Express Scripts, one of the largest pharmacy benefit managers in the country, for roughly $67 billion, integrating the management of drug coverage directly into the insurer's operating model. Both deals reflected the same conviction: that in capital-intensive, fragmented health markets, vertical integration is an operational strategy for reducing friction, aligning incentives, and improving margins across the care continuum. In pharma and healthcare delivery, this could mean closer integration between manufacturers, distributors, technology platforms, and providers.

Second, regional partnerships can enable expansion beyond single markets, particularly as companies seek to build scale across fragmented African healthcare systems. Third, acquisitions should be viewed not only as exit pathways, but as deliberate strategies for growth and market entry. This dynamic is already emerging. In 2021, Nigerian healthtech company Helium Health acquired Meddy, a Qatar-headquartered and UAE-based doctor-booking platform. This acquisition enabled Helium to expand beyond Africa into operating in the Gulf Cooperation Council (GCC) while integrating its electronic medical records and financial tools with Meddy’s patient-facing platform. More broadly, the ecosystem is starting to see early signals of mature exit pathways. LeapFrog Investments’ exit from Goodlife Pharmacy, one of East Africa’s largest pharmacy chains, is widely regarded as the largest private equity-backed healthcare retail exit on the continent to date.

As discussed in Season 1, Episode 3 of The Cure, where Dr Neto and Temitope Coker explored funding and scaling pathways in healthtech, these examples point to a critical shift. Private-private partnerships and strategic acquisitions will not only drive growth, but also create credible exit pathways for investors. For African healthcare to scale meaningfully, the ecosystem will need more of these outcomes where companies are built to scale, integrate, and ultimately exit, recycling capital back into the system.

Across all three industries, the pattern is clear. Scale is rarely achieved in isolation. It is built through partnerships that combine capital, capability, and market access. For healthcare, embracing this model may be one of the most important shifts required to move from fragmented pilots to system-wide scale.

Conclusion: We’ve Done This Before

If there is one thing this analysis makes clear, it is that healthcare in Africa is, in practice, a capital-intensive industry. The scale of infrastructure required creates real barriers to entry and long timelines for return. But this is not a reason for pessimism. It is a reason for hope and intentionality. Because while the challenge is significant, it is not unfamiliar.

Even within one market—Nigeria—these three capital giants reveal a range of strategies that have unlocked scale: diversified funding models, policy frameworks that enable private participation, and partnerships that combine local presence with global capability. And this is only a starting point. If so much can be learned from just three industries in one country, there is likely an even richer set of lessons across other sectors and markets on the continent.

We have built oil pipelines across difficult terrain. We have localised oil refining when it was once considered out of reach. We have distributed Coca-Cola, Fanta, and Maltina to the most remote villages. We have put GSM phones and smartphones into millions of hands, supported by digital financial services like OPay and PalmPay that reach deep into the informal economy. Why can’t insulin be just as accessible?

We’ve done this before. The blueprint exists. Now it’s time to apply it to healthcare.